Introduction:

The outlook for the Middle East remains highly uncertain, with ongoing disruption from logistical constraints, higher oil prices, and elevated geopolitical risk likely to persist until there is clear de-escalation. Markets have already priced in the inflationary impact of higher energy costs, pushing rates higher. In the U.S., Morgan Stanley has raised its 2026 inflation forecast from 2.6% to 3.2% and pushed expected Fed rate cuts (50bps) into the second half of 2026.

Oil prices may remain elevated for longer, reflecting both damage to regional production capacity and the need to replenish oil reserves, with potential spillovers to the broader macro cycle through weaker demand and possible production curbs. Consistent with this, Morgan Stanley has reduced its US GDP forecasts by 30bps to 2.3% in 2026 and 2.1% in 2027, from 2.6% and 2.4% respectively.

This backdrop favors real estate credit strategies that deliver above average returns, durable income, and downside protection, particularly in sectors supported by long term structural demand

Real Estate Fundamentals

Real estate fundamentals should benefit from a further pullback in supply. Rising energy linked inputs such as diesel, petrochemicals, and logistics costs are increasing construction expenses and impairing development feasibility, reinforcing the existing supply slowdown, delaying new starts, and supporting rent growth for standing assets. Additionally, real estate’s alignment with long term structural themes, including demographics and deglobalization, continues to provide stability during periods of volatility, alongside an intensified focus on energy efficiency and renewable solutions.

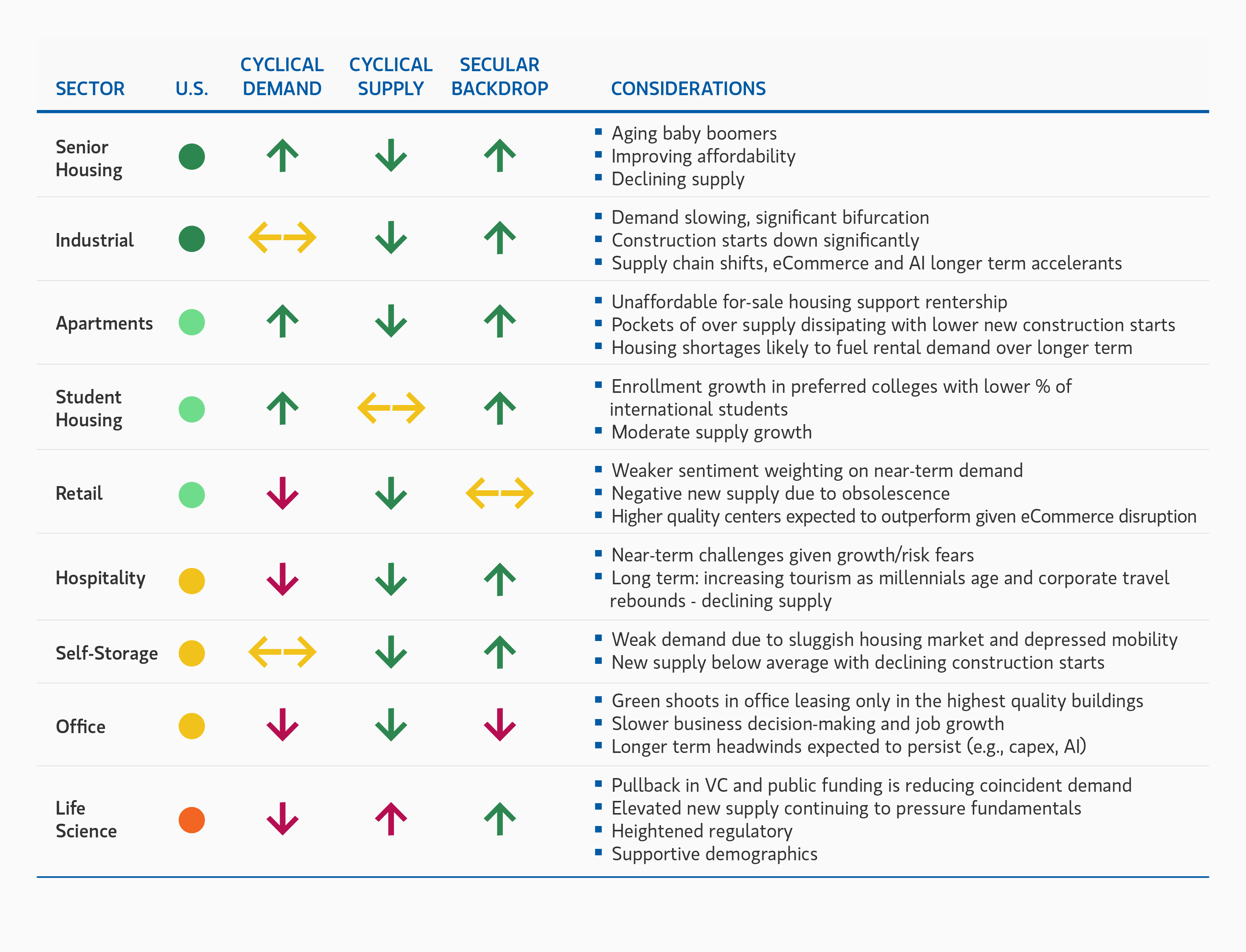

At the sector level, industrial assets are likely to be relative beneficiaries as supply chain resiliency, defense spending and inventory buffering drive incremental demand, though near term headwinds may emerge from higher shipping and energy costs, particularly for smaller transportation-oriented tenants and port proximate assets. Residential real estate should remain the least impacted overall given housing’s needs-based nature and rising mortgage rates that exacerbate for sale affordability challenges, although lower income segments are more sensitive to energy driven inflation. As an extension to traditional multifamily, both senior living and student housing sectors should continue to remain attractive. While higher energy costs may pressure margins for senior living operators in the near-term, strong top-line growth driven by the rapid expansion of the baby boomer cohort and continued low supply should support outsized NOI growth.

Additionally higher in-place yields provide an additional cushion against a higher interest rate environment. In student housing, demand has historically proven resilient during periods of economic stress, as students often delay entering the workforce and pursue higher education. Importantly, demand is driven by enrollment rather than discretionary consumer spending, supporting rent durability across cycles.

Real Estate Capital Markets

The risk reward profile in real estate has shifted away from macro policy uncertainty toward an environment increasingly shaped by elevated and volatile geopolitical risk, as magnified by the war in Iran. Against this backdrop, increased market volatility is likely to push investors toward more defensive positioning, including hard assets that offer inflation protection with durable income and credit opportunities that offer downside protection. With property values having adjusted by roughly 25%, new loans are now being originated against more conservative valuations, enhancing downside protection while maintaining attractive yields relative to other fixed income alternatives.

Markets are likely to remain headline driven in the near term as investors differentiate between a temporary shock and a more prolonged energy disruption, with uncertainty potentially delaying real estate investment activity and driving a flight to quality across global portfolios. At the same time, higher inflation has anchored expectations for elevated interest rates, while a risk off environment could drive wider credit spreads, supporting higher all in real estate debt returns.

Real estate credit may also benefit from capital rotating away from corporate private credit strategies where some valuations have come under pressure. Loans secured by income producing real estate offer tangible collateral, enforceable security, and often inflation linked cash flows—downside protections that are largely absent in many corporate or technology-oriented credit strategies. As volatility rises and regulatory scrutiny persists, banks and traditional lenders may retrench and tighten underwriting standards, creating opportunities for alternative lenders to capture a greater share of new originations and refinancings.

Conclusion

While the current macro and geopolitical backdrop introduces additional risk, real estate is positioned to outperform as an asset class given already compressed valuations, durable income streams, inflation hedging characteristics, and alignment with long term structural demand drivers. Within real estate, private credit offers particularly attractive risk adjusted returns, supported by subordination that provides incremental downside protection. Ultimately, outperformance will depend on managers’ ability to construct diversified portfolios across markets, property types, and sponsors, while maintaining a granular, disciplined, and highly selective underwriting approach.

Vorgestellte Einblicke