The conflict in the Middle East has sent shockwaves through global markets, with higher oil prices and increasing inflation creating a volatile environment. The tipping point between events in the Gulf and markets is a function of time. More specifically, we need to understand whether the rise in energy prices is merely transient, or will be sustained long enough to become embedded in broader economic activity and expectations.

If elevated energy prices persist, the knock-on effects would be significant, potentially resulting in a growth scare. Sustained high prices would decrease demand, weaken growth expectations and ultimately weigh on valuations, all leading to a significant negative impact on global markets. The steep backwardation in the oil futures curve (where the price of a futures contract in oil is trading below the expected spot price at contract maturity) points to lower prices over time, but also signals future supply shortages at levels that maintain growth buoyancy and away from a growth or valuation shock.

Despite these concerns, the current situation is likely to be a price shock, not a valuation shock, suggesting a dislocation, not deterioration, and an opportunity to reestablish growth strategies at lower prices. At the onset of the conflict, even prior to the April 8 ceasefire, markets had priced inflation as a shock rather than a growth scare. This initial reaction was shaped by market conditions going into the event, which in this case were quite strong.

Until the Iran Conflict Ends, Oil Remains the Focal Point for Markets

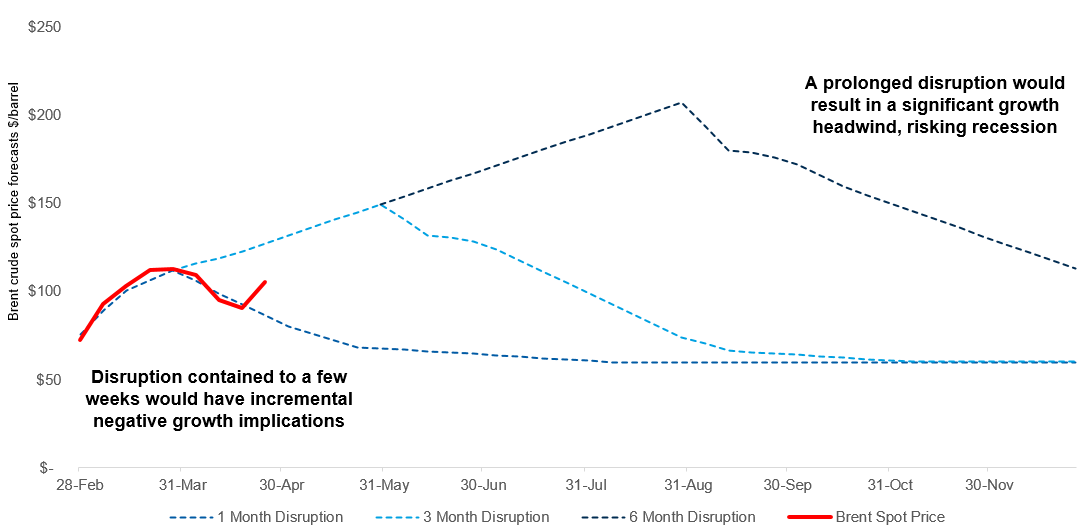

Hypothetical Scenarios for the Strait of Hormuz Closure

Until the Iran Conflict Ends, Oil Remains the Focal Point for Markets

Hypothetical Scenarios for the Strait of Hormuz Closure

Display 1

Why Did U.S. Equity Prices Rise Despite Persistent Geopolitical Risks

We get this question a lot - and seems to divide investors. Our explanation is that at the start of the war markets were in a period of ambiguity, but have now morphed into utter uncertainty. What’s the difference? Well, at the start of a conflict, markets can’t model ambiguity because it’s hard to clearly see the paths ahead through the fog of war. Now that there is a better comprehension of the conditions, uncertainty takes over, something markets can model and manage, thereby lowering the risk premia. Let me explain.

When Epic Fury began, investors were naturally unclear about how things would proceed. As such, risk was quickly reduced, as they believed downside (left-tail) risks largely outweighed the upside (right-tail) risks. Because the left tail was fatter than the right tail, the balance point of the distribution finished at a lower price.

Time has passed and now there is a better understanding of the shape of the war. In my mind, Epic Fury has turned into Economic Fury, as coercive policies will be set through economic means. For example, the Strait of Hormuz blockade is viewed by the market as a reduction in left-tail risk and a corresponding increase in right-tail risk, thus raising the market price balance point. This was pushed even higher given the recent strength in earnings.

To be sure, markets fully appreciate the risks in the current environment. However, they are also currently exploring the upside possibilities, not just obsessed with the downside. This pushes the balance point of the uncertainty distribution to land on higher prices.

Market Impact and U.S. Resilience

In the U.S., while the conflict provides near-term volatility, fiscal stimulus from the One Big Beautiful Bill Act, deregulation and AI adoption all remain supportive of growth, providing the foundations of a positive outlook for the balance of 2026.

Against this backdrop, markets were primed for a quick war resolution to be the impetus for oil prices to revert to pre-war lows, with an incremental negative growth impact. After the ceasefire was announced – including the temporary reopening of the Strait of Hormuz - Brent crude initially dropped 16% before recovering to 13.5% at $94.36 (as of April 21, 2026). Notably, prices still remain above where they were before the start of the conflict, when Brent traded below $73 a barrel.

The initial market rebound doesn’t signify a linear recovery, as volatility is likely to be stubborn, with negotiations for a lasting peace expected to rumble on.

Higher Energy Prices May Linger Longer

Given the heightened volatility war injects into oil and gas markets, and the fact that oil prices are unlikely to hit their pre-conflict lows, energy security has unsurprisingly become top-of-mind for global governments. The impact on inflation is likely to be higher than what oil prices alone suggest, reflecting a widening spread between crude and refined products such as gasoline and diesel. This points to intense price pressure “at the pump,” adding an additional inflationary concern for consumers.

High Oil Prices: Inflation Shock (Price) vs. Growth (Valuation)

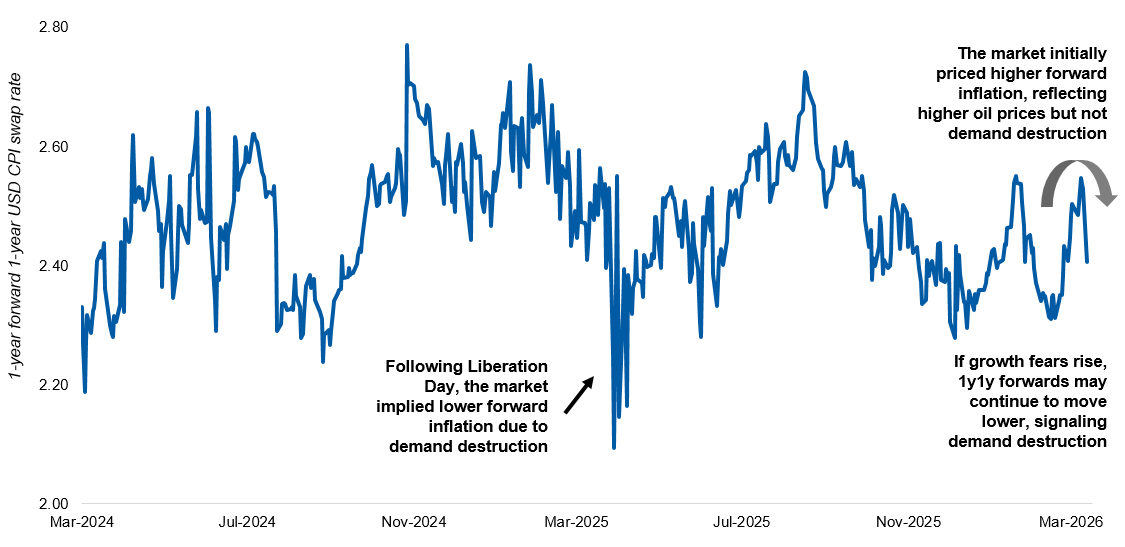

The 1y1y* Inflation Swap Does Not Show a Clear Demand Destruction Signal…Yet

High Oil Prices: Inflation Shock (Price) vs. Growth (Valuation)

The 1y1y* Inflation Swap Does Not Show a Clear Demand Destruction Signal…Yet

Display 2

Regional Disparities

In the U.S., consumers entered the oil shock from a position of balance sheet strength. Heading into the current oil spike, energy’s share of household spending sits near the historical low end of the range, providing a meaningful buffer that should help insulate consumer demand and the broader economy.

In contrast, Europe relies heavily on imported energy and is particularly susceptible to energy shocks, where inflation responds more sharply than in other regions. Until recently Europe had been in a relatively constructive macro position, with inflation easing, activity stabilising and fiscal policy - particularly in Germany and France - beginning to provide a modest growth impulse after a period of political and fiscal uncertainty.

Despite this relatively constructive position, the Iran conflict has served as another reminder that investments to reduce reliance on external sources of energy need to be a key part of the agenda for European policymakers moving forward, where the region will benefit from a strong push to expand energy grids and boost renewable capacity. This dependence means that Europe will be saddled with residually higher energy costs for longer, as global energy prices are unlikely to fall significantly from current levels anytime in the near future.

The conflict has also exposed Asia’s energy dependence across crude oil, gas and refined petroleum, all of which are heavily reliant on Middle East supplies. Similar to other regions, before the conflict started Japan benefitted from strong domestic tailwinds, underpinned by fiscal stimulus, corporate governance reforms, domestic reflation and a gradual normalisation of BoJ policy. Energy remains a consequential vulnerability for Japan given its import dependence, though it is likely to have a less acute impact than in Europe in terms of recovery.

Dislocation Is an Opportunity

The Iran conflict has delivered a price shock, not a valuation shock. Volatility will likely remain dogged as peace negotiations continue, where the underlying strength of global markets, particularly in the U.S., suggests resilience rather than deterioration. For investors, we believe this dislocation presents an opportunity to re-establish growth strategies at more attractive entry points.

Regional disparities will certainly remain, with Europe and Asia facing prolonged energy cost pressures, while the U.S. benefits from its position as a net energy exporter. Moving ahead, investing requires continued vigilance, but the foundations for recovery are already intact. Disciplined positioning and a focus on structural growth drivers will be crucial in navigating the path forward.

Featured Insights